DeFi and bonding go together like water and oil. Tight jeans and Thanksgiving dinner. Discrete math and concussions.

To be a bit more clear, floating rate bonds don’t make sense in an industry as volatile and accessible as crypto. Whether Curve’s voting escrow, Olympus’ (3,3), or some other bonding system, these complex financial instruments are often sold to laymen as a means of creating exit liquidity, advertising inflated short-term APYs to get users locked in for the long haul.

DeFi asset lockers are down bad right now, with veCRV users boasting less APR over the past 2 years than the current risk-free rate of ~4%, even ignoring underlying capital losses. Convex and similar protocols have worked to unlock escrowed assets for users, but the cost is the system’s original value proposition and an unsustainable cycle of value extraction.

Where bonding skews incentives toward the protocol at the cost of elasticity and value for users, the alternative paradigm puts power squarely in the hands of mercenary capital at the cost of solvency, sustainability, and dignity.

I’m talking of course about liquidity mining. Pioneered by Synthetix and Compound and popularized by Sushiswap’s MasterChef system, the idea behind liquidity mining is simple: users deposit an asset into a smart contract and receive a set amount of tokens for every block their assets are staked.

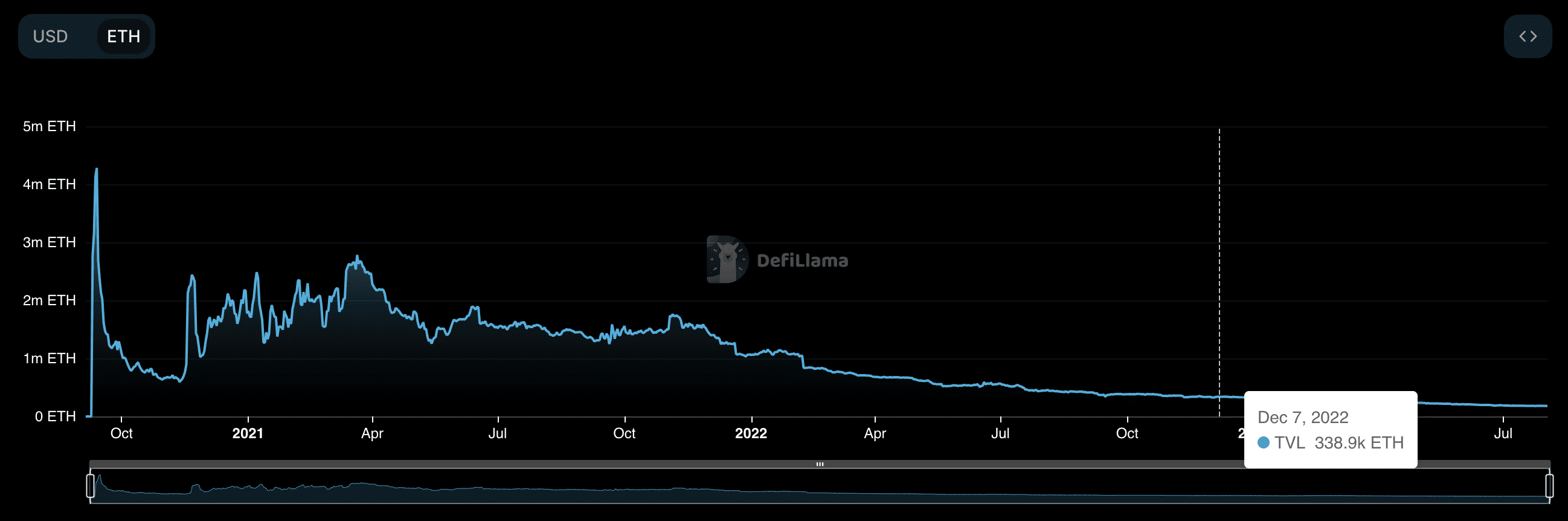

In long time frames, results of liquidity mining programs usually range from sad to catastrophic, with liquidity providers extracting as much value as possible before withdrawing and moving onto the next thing. Without incentive to stick around, these systems rely on speculators continuously moving in to stanch the bleeding as token prices and liquidity race toward 0.

Sushi TVL —showing a common trend in liquidity mining.

Our team created Reliquary as a DeFi-native solution to the problems introduced by current incentive systems.

Through Reliquary, we seek to find a middle-ground between bonding and liquidity mining, with the protocol-level benefits of the former and elasticity of the latter. The result resembles a liquid floating-rate bond which increases in convexity over time, aligning the protocol with its liquidity providers better than ever before.

Put simply, the longer you remain in a Relic, the more incentives you’ll receive. This means the best liquidity providers will receive the largest share of rewards.

These rewards are distributed across Maturity Tranches, each of which represents a length of time a user will receive a certain level of incentives. This is done in a non-dilutive fashion, with the same amount of rewards always being emitted to the pool no matter how many users are in any tranche.

This maturity system allows developers to program desired holding patterns into each pool, giving them unparalleled control over their incentive structures. Additionally, each user is issued a custom NFT for use in external protocols: they can lock it, lend it, or sell it on their favorite marketplace to earn a premium on their time spent in the pool.

The best part of it all? Users can withdraw at any time. Though with built in airdrop mechanics, multi-asset rewards, and maturity bonuses, why would they ever want to?

In typical Byte Masons style, we’re solving problems simply by adding value. Reliquary is an open-ended, 3x audited platform with a plugin system and suite of tools that will supercharge any incentive program. We’ve been testing with a small group of users and will soon run a short incentive program for another group of testers.

Related Posts

Digit: An Internal Post Beta Review

Covering key statistics and features from the BETA release, lessons learned…